GP Stakes

Discover the benefits owning a stake in private asset management firm

A GP Stake involves the purchase of a minority and passive interest in a Private Equity (or Private Credit) firm, allowing investors to access the long-term success and growth of the firm itself.

Overview

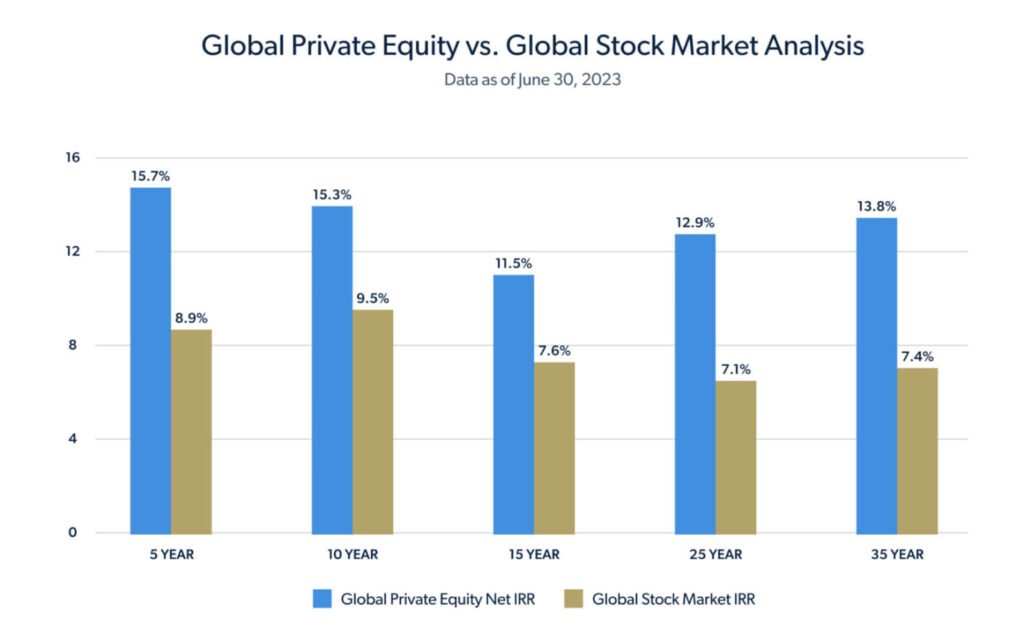

Between 1986 and mid 2023 (6/30/23), U.S. Private Equity as an asset class produced average annual returns of 14.3% while the S&P 500 produced 9.5% percent. That’s nearly 50% greater compounded annualized returns. On a global level, private equity has outperformed global stock markets over various time periods over the last 35 years. This performance has driven trillions of dollars of investment into private asset managers who benefit greatly from the management fees and performance fees they collect.

Another key driver for the future of Private Equity is that fewer companies are going public. The number of publicly traded U.S. companies has fallen by nearly half, from over 8000 in 1996 to less than 3800 today. Today, approximately 87% of companies with over $100 million in annual revenue remain privately held.

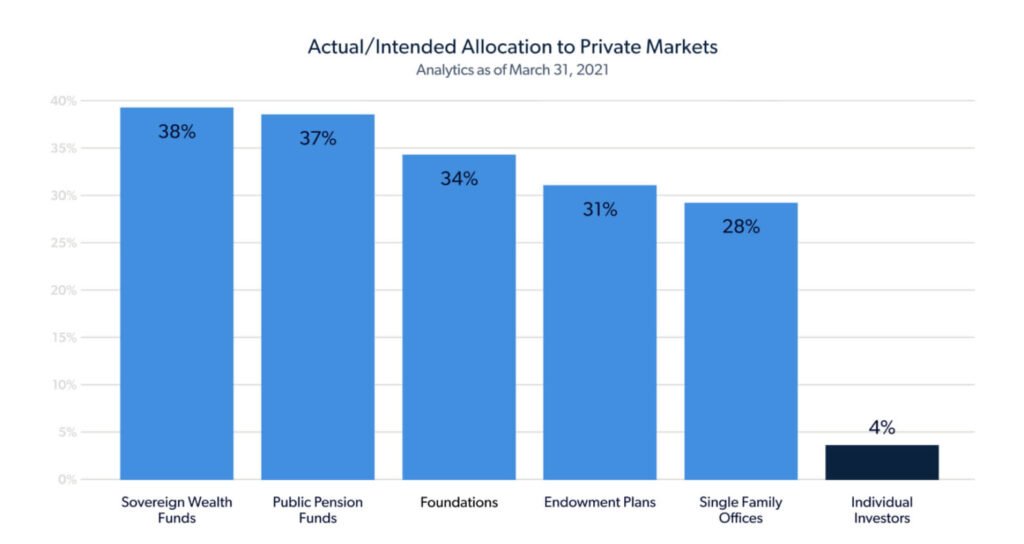

This is changing dramatically as people seek out uncorrelated investments like Private Equity, Private Credit and Private Real Estate, to complement their traditional stock and bond portfolios. This democratization of alternatives is predicted to cause trillions in new capital to flow into alternative investment managers.

Taking Advantage of Private Market

How does one take advantage of this massive shift toward the private markets? One approach is a category called “GP Stakes.” This entails owning a minority stake or interest in the actual asset management company that is managing investors’ money within Private Equity, Private Credit, Venture Capital and Private Real Estate. These are known as the General Partners or GP’s in a typical fund structure.

These asset managers generate revenue by charging their investors (the limited partners of LPs’) two separate fees: management fees and performance fees. Like the shareholders of any business, the owners of a GP stake get to share in the profits on a pro rata basis.

So why can it be more attractive to be a GP, a General Partner, than an LP, a Limited Partner?

A typical asset management company manages numerous fund vehicles on behalf of investors, the LP’s. The investors often agree to “lock up” their investments for longer periods of time in exchange for the potential of outsized returns.

This can generate predictable cash flow for the firm and it’s GP stake owners. In addition, the GP receives a handsome percentage of the profits, typically 20 percent, on all the capital they manage. This can be quite significant if the funds they manager perform well.

Lastly, GP stakes owners receive significant diversification. The LPs choose to invest in each individual fund vehicle (or “vintage”) whereas the GP is the manager of all the company’s funds, past, present and future. Each of those funds has a unique start date or “vintage,” which means they are spread across various market/economic cycles. Beyond that, each of those funds contains its own portfolio of companies/ investments spread across various industries, sectors, geographies, and stages of growth.

If you zoom out, the global total allocation to alternative investments is approximately $25 trillion. This is estimated to grow to $60 trillion by 2032. This is why we believe that GP Stakes is an ideal strategy to take advantage of these significant tailwinds.

Highlights

- Between 1986 and 2022, the Private Equity asset class has significantly outperformed the S&P 500 (14.28% vs 9.24%)

- 87% of companies with over $100 million in annual revenue are private as fewer companies are opting to go public

- The number of publicly traded U.S. companies has fallen by nearly half to around 3,800, since the peak in 1996